TL;DR

- Robo-advisors automate tax-loss harvesting - a strategy that was once exclusive to wealthy investors

- One user earned $264 in tax savings on a $15K portfolio, exceeding the $55 annual management fee

- Algorithms scan portfolios daily and execute tax-saving trades in seconds

- Best for: Taxable investment accounts (not IRAs/401ks) with long-term investment goals

- Key benefit: After-tax returns improve 1-2% annually through automated optimization

Robo-advisors like Wealthfront now give everyday investors access to tax-loss harvesting - a strategy that once required $10,000+ wealth management fees - delivering real tax savings that exceed the platform’s cost.

When David’s financial advisor mentioned “tax-loss harvesting,” David nodded politely.

He had no idea what it meant. He assumed it was one of those fancy strategies rich people used - complicated, requiring teams of accountants, not for regular investors like him.

Then he opened a Wealthfront account with $15,000 of savings.

Within a year, the algorithm had harvested $1,200 in tax losses he never would have captured himself. Money that would have gone to the IRS instead went back into his portfolio.

David didn’t do anything. The robot just… did it.

The Strategy Nobody Could Execute

Tax-loss harvesting is simple in theory:

- You own an investment that has dropped in value

- You sell it, “realizing” the loss

- That loss offsets your taxable gains (or up to $3,000 of regular income)

- You immediately buy a similar (but not identical) investment to maintain your market position

- You’ve locked in a tax benefit without actually changing your portfolio exposure

Here’s why regular people never did it:

Monitoring: You’d need to check your portfolio daily to catch opportunities.

Speed: Markets move fast. By the time you notice a dip, it might have recovered.

Wash sale rules: The IRS says you can’t buy the same security within 30 days or you lose the tax benefit. You need a “substantially different” replacement - but what qualifies?

Transaction costs: In the old days, each trade had commissions. Frequent selling was expensive.

Complexity: Tracking which lots you bought when, which have losses, which replacements to use - it’s spreadsheet hell.

Human investors rarely bothered. The strategy was theoretically great but practically impossible.

Enter the algorithm.

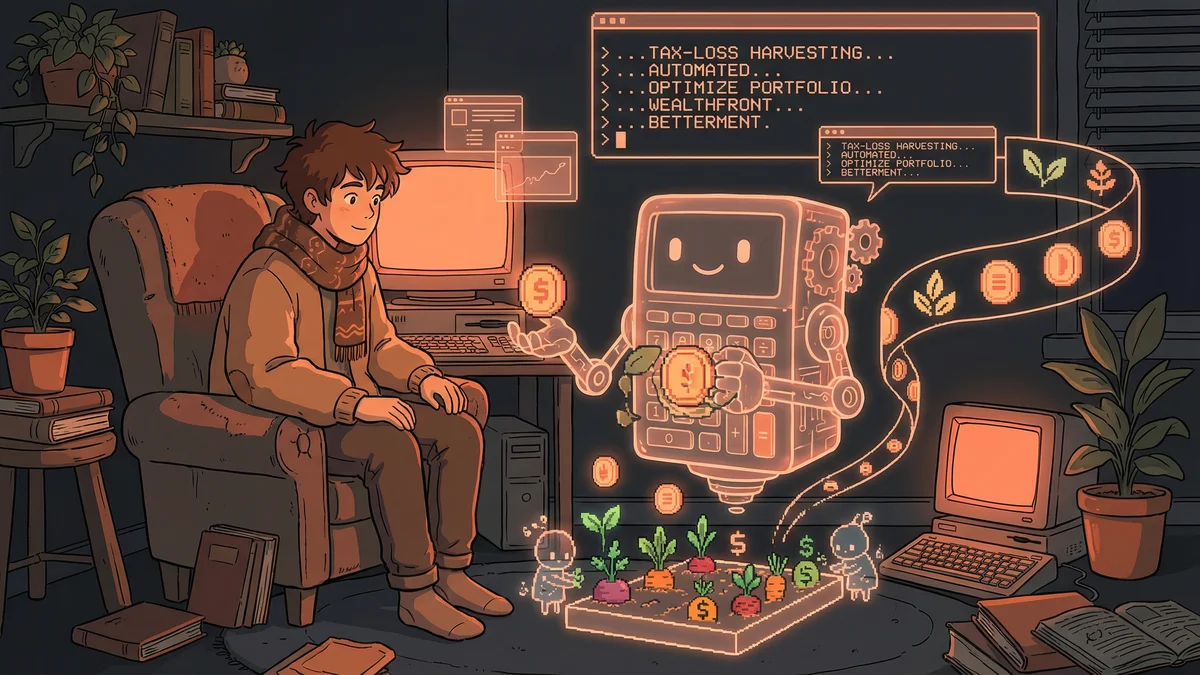

What the Robot Does

Robo-advisors like Wealthfront and Betterment run tax-loss harvesting automatically:

Daily scanning: The algorithm checks every holding in your portfolio every day, looking for losses to harvest.

Instant execution: When a loss is identified, the robot sells immediately and buys a replacement ETF in seconds.

Wash sale compliance: The algorithm knows exactly which replacements are “substantially different” enough to be legal.

Across-portfolio coordination: If you have multiple accounts, the algorithm coordinates to avoid accidental wash sales.

Year-round operation: This isn’t just a December thing. The robot harvests losses whenever they appear, maximizing opportunities.

David’s portfolio had 5 tax-loss harvesting events in his first year. Each one was tiny - $200 here, $350 there. But they added up.

More importantly, he did nothing. He didn’t know the events happened until he saw the tax report.

The Alpha Nobody Talks About

Investment returns are often compared to benchmarks. If the S&P 500 returned 10% and your portfolio returned 10%, you didn’t beat the market.

But tax-loss harvesting creates a different kind of edge: after-tax alpha.

If the S&P returned 10% and your portfolio returned 10% but you also reduced your tax bill by 1-2% through harvesting, your actual financial position improved more than the raw return suggests.

Studies suggest tax-loss harvesting can add roughly 1-2% in annual tax savings for taxable accounts. That doesn’t sound like much, but compound it over 20 years and it’s meaningful.

The key insight: this “alpha” was previously only available to people who could afford wealth managers charging $10,000+/year or who had family offices monitoring their portfolios.

Now it’s available to anyone with a Wealthfront account and a 0.25% management fee.

David’s First Year

Starting balance: $15,000 Annual contribution: $500/month End balance: $21,800

Tax losses harvested: $1,200 Estimated tax benefit (22% bracket): $264

The $264 in tax savings exceeded Wealthfront’s management fee ($55 on his average balance).

The service literally paid for itself through tax efficiency alone - before even considering whether his investments performed well.

What Else the Robot Does

Tax-loss harvesting is the headline feature, but robo-advisors automate several other things:

Rebalancing: When your portfolio drifts from target allocation (say, stocks grow faster than bonds), the algorithm sells high and buys low automatically.

Dividend reinvestment: Every dividend gets immediately reinvested according to your target allocation.

Direct indexing (newer): Instead of owning an S&P 500 fund, you own the underlying 500 stocks directly - which creates even more tax-loss harvesting opportunities.

Tax-efficient withdrawal: When you need money, the algorithm sells from the most tax-efficient lots first.

Each of these is something a skilled financial planner would do. The robot just does them continuously, without forgetting, without vacations, without hourly fees.

The Limitations

Robo-advisors aren’t magic. Important caveats:

Only taxable accounts benefit: Tax-loss harvesting does nothing in IRAs or 401(k)s since those accounts aren’t taxed annually anyway.

You need losses to harvest: In a year when everything goes up, there’s nothing to harvest. The strategy works best in volatile or down markets.

Not investment advice: Robo-advisors optimize execution, not strategy. If your investment allocation is wrong for your goals, the robot will efficiently execute the wrong strategy.

No holistic planning: A human advisor would ask about your life, your goals, your estate plan, your insurance. Robots just manage the portfolio.

Behavioral risks: Some people panic-sell during downturns. Having a robot won’t stop you from overriding it emotionally.

The Human Element Isn’t Gone

David still checks his portfolio. He still has questions. But his questions changed.

Before: “What should I buy? When should I sell? Am I doing this right?”

After: “Is my overall allocation appropriate for my age? Should I increase contributions? Do I understand what I’m invested in?”

The robot handles the operational complexity. David handles the strategic decisions about his life.

When he had questions beyond the robot’s scope - like whether to prioritize mortgage payoff vs. investing - he used ChatGPT to think through scenarios. The AI walked him through the math of both approaches and helped him understand the trade-offs.

Between the robo-advisor and the AI assistant, David felt more confident about his finances than ever, despite having zero formal financial training.

The Broader Democratization

Wealth management used to work like this:

- Under $100k: You’re on your own with a brokerage account and Google

- $100k - $1M: Maybe you can afford a fee-only advisor occasionally

- $1M+: Now you get real wealth management with sophisticated strategies

Robo-advisors collapsed this hierarchy.

For $15,000 and a 0.25% fee ($37.50/year), David gets:

- Automated portfolio management

- Tax-loss harvesting

- Automatic rebalancing

- Tax-efficient placement

It’s not identical to what a billionaire gets. But it’s closer than anything before.

David’s Reflection

“I used to think investing was for people who knew what they were doing. I’d buy random stocks, panic-sell when they dropped, keep cash in savings accounts earning nothing.

The robo-advisor removed me from my own worst impulses. It just… invests. Efficiently. Without drama. And it does the tax stuff I would never have done myself.

I don’t think about my investments anymore. They just grow, and once a year I get a tax benefit I didn’t earn.

That’s what technology is supposed to do - make the optimal thing automatic.”